The seller tells you the embalmer is a contractor. The removal driver is a contractor. The hairdresser who comes in three times a week is a contractor. It keeps payroll clean and taxes low. But when you buy this business, every one of those classification decisions becomes your problem — and the IRS, your state labor department, and the Department of Labor do not care what the seller told you.

The Classification Problem Nobody Mentions in Funeral Home Due Diligence

Worker misclassification is one of the most common — and most expensive — hidden liabilities in funeral home acquisitions. It rarely surfaces during initial conversations with the seller, and most buyers never think to ask.

Here is what happens in practice. A funeral home owner needs a part-time embalmer two or three days a week. Hiring that person as a W-2 employee means paying the employer share of FICA (7.65%), unemployment insurance premiums, workers’ compensation coverage, and potentially offering benefits. Classifying the embalmer as a 1099 independent contractor eliminates all of that overhead in one stroke.

So the owner issues a 1099. The embalmer shows up on a schedule set by the funeral home, uses the funeral home’s prep room and chemicals, follows the funeral home’s procedures, and works primarily for that one funeral home. Everybody pretends it is a contractor relationship. It is not.

The roles most commonly misclassified in funeral homes include:

- Part-time embalmers — brought in for overflow or to cover days the full-time embalmer is off

- Removal and transport drivers — on-call staff who pick up decedents from hospitals, nursing homes, and residences

- On-call night staff — people who answer the after-hours phone and respond to death calls

- Hairdressers and cosmetologists — brought in to prepare decedents for viewing

- Musicians and officiants — organists, soloists, or non-clergy celebrants used regularly

The financial incentive is real. For a worker paid $40,000 annually, the employer saves roughly $6,000–$8,000 per year by classifying them as a contractor instead of an employee. Multiply that across three to five misclassified workers and the seller has been saving $20,000–$40,000 annually — savings built on a classification that almost certainly fails under legal scrutiny.

The exposure is equally real. Three to five misclassified workers over a three-year lookback period can generate $50,000 to $150,000 or more in back taxes, penalties, and interest. That liability does not disappear when you sign the purchase agreement.

The ABC Test and Why Most Funeral Home Contractor Arrangements Fail

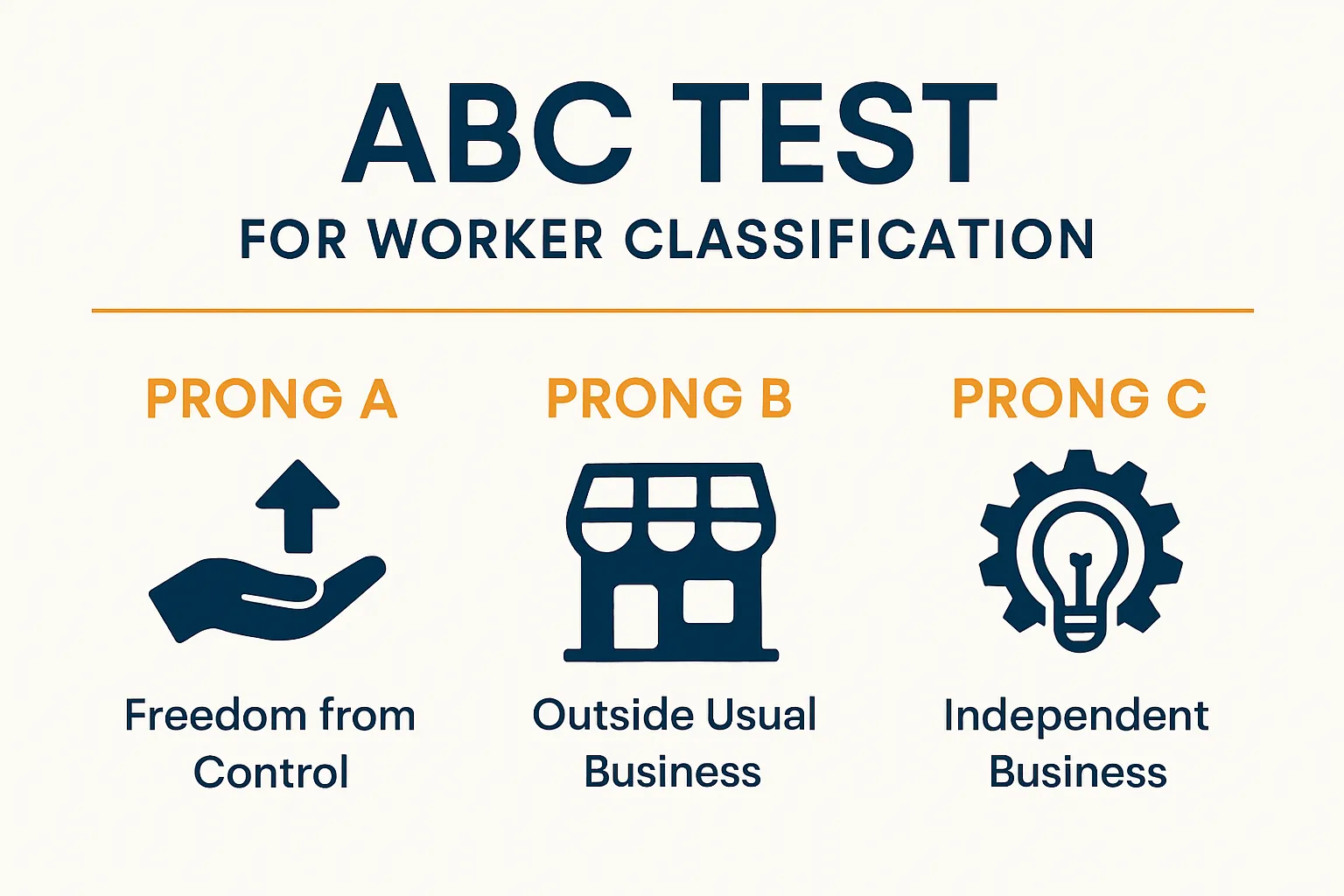

The legal standard for worker classification varies by jurisdiction, but the dominant framework is the ABC test, now used by approximately 30 states and increasingly favored by the U.S. Department of Labor. Under the ABC test, a worker is presumed to be an employee unless the hiring entity proves all three of the following:

Prong A: Freedom from Control and Direction

The worker must be free from control and direction in performing the work, both under the contract and in fact.

Funeral homes fail this prong routinely. The funeral home sets the embalmer’s schedule based on when bodies need preparation. The funeral home dictates embalming procedures, chemical usage, and restoration standards. The removal driver uses a funeral home vehicle, follows funeral home protocols for body transport, and reports to the funeral home’s dispatch. The hairdresser comes in when the funeral home calls and prepares the decedent according to the family’s instructions relayed by the funeral director.

Control is baked into how funeral homes operate. You cannot run a funeral home without directing how and when work gets done.

Prong B: Outside the Usual Course of Business

The worker must perform work that is outside the usual course of the hiring entity’s business.

This is the prong that destroys most funeral home contractor arrangements. Embalming is the funeral home’s business. Body removal and transport is the funeral home’s business. Preparing decedents for viewing — including hair and cosmetics — is the funeral home’s business. These are not peripheral activities. They are core service delivery.

A funeral home could plausibly argue that a plumber who fixes a broken pipe is an independent contractor under Prong B. It cannot credibly argue that the person embalming bodies is performing work outside the funeral home’s usual business.

Prong C: Independently Established Trade or Business

The worker must be customarily engaged in an independently established trade, occupation, or business of the same nature as the work performed.

Most part-time funeral home workers do not operate independent businesses. They do not have their own clients, their own prep rooms, their own equipment, or their own business insurance. They work for one funeral home — sometimes two — and they find that work through personal relationships, not through marketing an independent business to the public.

A truly independent trade embalmer who serves multiple funeral homes across a region, carries their own liability insurance, sets their own rates, and markets their services independently might pass this prong. The part-time embalmer who has worked exclusively at one funeral home for seven years does not.

The IRS 20-Factor Test

In states that have not adopted the ABC test, the IRS applies a 20-factor test (now condensed into three categories: behavioral control, financial control, and type of relationship). The IRS test is somewhat more flexible than the ABC test, but funeral home arrangements still fail it frequently because of the degree of behavioral control inherent in funeral service operations.

Roles That Almost Always Fail Classification Tests

Some funeral home roles have virtually no defensible basis for contractor classification:

- Removal drivers using funeral home vehicles — the funeral home provides the vehicle, sets the route, and controls the timing

- Part-time embalmers working at the funeral home’s prep room on the funeral home’s schedule — control, location, equipment, and core business all point to employment

- On-call night staff — required to be available during specific hours, respond to calls within a defined timeframe, and follow funeral home protocols

- Regular hairdressers/cosmetologists — if they come in on a recurring basis at the funeral home’s request, use the funeral home’s facilities, and serve the funeral home’s clients

The only funeral home contractor arrangement that typically withstands scrutiny is a genuinely independent trade embalmer or trade services firm that operates as a standalone business, serves multiple funeral homes, and maintains their own insurance and professional licensure.

What the Buyer Inherits

Understanding the liability is one thing. Understanding who bears it after closing is what matters for your acquisition.

Asset Purchase vs. Stock Purchase

In a stock purchase (or membership interest purchase for an LLC), you acquire the legal entity itself — including all of its historical tax liabilities. Every misclassification decision the seller made for the life of the entity is now your problem. There is no ambiguity.

In an asset purchase, the analysis is more complex but the outcome is often the same. Many states impose successor liability on asset purchasers, particularly for unpaid employment taxes and unemployment insurance contributions. The IRS can also pursue successor liability claims against asset purchasers under certain circumstances.

Do not assume that structuring the deal as an asset purchase insulates you from the seller’s misclassification exposure. It may reduce it, but it rarely eliminates it. Your due diligence checklist should include worker classification review regardless of deal structure.

IRS Section 530 Relief

Section 530 of the Revenue Act of 1978 provides a safe harbor for employers who have a reasonable basis for treating workers as independent contractors. This relief requires a consistent filing history and reliance on a reasonable basis (such as industry practice, prior IRS audit, or legal/accounting advice).

Here is the problem for buyers: Section 530 relief is entity-specific. Even if the seller qualifies for Section 530 relief based on their historical practices, that relief does not transfer to you as the new owner. You start fresh, and any forward-looking classification decisions are evaluated on their own merits.

The Penalty Math

When the IRS reclassifies a 1099 contractor as an employee, the penalties stack:

- 100% of the employee’s unpaid share of FICA (6.2% Social Security + 1.45% Medicare) for the lookback period

- The employer’s share of FICA — normally 7.65%, but assessed at a penalty rate

- Federal income tax withholding — assessed at 1.5% of wages if no 1099 was filed, or 20% of wages in some cases

- Failure-to-file and failure-to-pay penalties on top of the base tax

- Interest running from the original due date

For a single worker paid $45,000 per year over a three-year lookback period, the combined federal exposure can reach $15,000–$25,000. Scale that across three to five workers and you are looking at $50,000–$125,000 before state-level exposure is added.

State-Level Exposure

States add their own layer of pain:

- Unpaid unemployment insurance contributions with penalties and interest

- Unpaid state income tax withholding (in states with income tax)

- Workers’ compensation penalties — if a misclassified worker was injured on the job, the exposure can be catastrophic

- State attorney general enforcement — multiple states have increased misclassification enforcement in 2025–2026, with several establishing dedicated task forces

The workers’ compensation angle is particularly dangerous. If a removal driver classified as a contractor is injured lifting a 300-pound decedent, and the funeral home has no workers’ comp coverage for that person, the funeral home faces both the injury claim and penalties for failure to carry required coverage. Review your staffing risk assessment with this scenario in mind.

How to Audit Worker Classification During Due Diligence

A thorough classification audit does not require a forensic accountant, but it does require deliberate effort. Here is the process.

Step 1: Request the 1099 Filing History

Ask the seller for three years of 1099-NEC filings (1099-MISC for years before 2020). This tells you who was paid as a contractor, how much they were paid, and how consistently the arrangement was maintained.

Red flags:

- A 1099 recipient who was previously a W-2 employee at the same funeral home (the IRS scrutinizes reclassifications heavily)

- 1099 recipients paid more than $30,000 per year (suggests a full-time or near-full-time relationship)

- Multiple 1099 recipients performing core funeral home functions

Step 2: Cross-Reference with Workers’ Compensation

Pull the funeral home’s workers’ comp policy and compare the covered employee list against the 1099 recipients. If the workers’ comp policy excludes people who are performing physical work at the funeral home — lifting bodies, driving vehicles, handling chemicals — that gap is a dual liability: misclassification exposure plus uninsured workers’ comp exposure.

This cross-reference is one of the fastest ways to identify classification problems. Learn more about evaluating the workers’ comp picture in our insurance coverage guide.

Step 3: Interview Key Workers

Talk to the people classified as contractors. Ask them:

- Who sets your schedule?

- Whose equipment do you use?

- Do you work for other funeral homes?

- Do you have your own business insurance?

- Can you turn down assignments?

- How did this arrangement start?

Their answers will tell you more about the true nature of the relationship than any contract on file.

Step 4: Review Independent Contractor Agreements

Many funeral homes issuing 1099s have no written contractor agreements at all. If agreements exist, review them for provisions that undermine contractor status:

- Non-compete clauses (contractors do not typically agree to non-competes)

- Requirement to attend training or meetings

- Specified hours or shifts

- Exclusivity provisions

- Funeral home-provided equipment or supplies

A well-drafted independent contractor agreement does not make someone a contractor. But a poorly drafted one — or the absence of one entirely — makes the misclassification argument even easier for regulators.

Step 5: Check for Prior Audits

Ask the seller directly: has the funeral home ever been audited by the IRS, state labor department, or state unemployment agency on worker classification issues? Has the seller ever voluntarily reclassified workers?

A prior audit with an adverse finding that was never corrected dramatically increases the exposure. A prior audit with a favorable finding provides some comfort — but remember, Section 530 relief does not transfer to buyers.

Negotiating the Risk

Once you have identified misclassification exposure, you have several options — none of which involve ignoring it.

Representations and Warranties

Your purchase agreement should include specific representations from the seller regarding worker classification. Generic “compliance with all laws” language is not sufficient. You need the seller to represent that:

- All workers are properly classified under federal and state law

- No worker currently classified as an independent contractor performs work that would require employee classification

- The funeral home has not received any notice of audit, investigation, or inquiry regarding worker classification

- No workers have been reclassified from employee to contractor status during the seller’s ownership

These representations create a contractual basis for indemnification if classification problems surface post-closing.

Indemnification Clauses

The indemnification section should explicitly cover pre-closing tax liability arising from worker misclassification, including:

- Federal and state employment taxes, penalties, and interest

- Workers’ compensation claims by misclassified workers

- Legal fees incurred in defending against classification audits

- Any settlement amounts paid to resolve classification disputes

The indemnification should survive closing for at least three years — matching the IRS lookback period — and ideally four years to cover the statute of limitations in most states.

Escrow Holdback

If the classification risk is significant, negotiate an escrow holdback sized to the potential exposure. A reasonable calculation:

- Identify total payments to potentially misclassified workers over three years

- Calculate combined federal and state tax exposure (typically 20–30% of total payments)

- Add penalties and interest (estimate 50% of the base tax)

- Hold that amount in escrow for 18–24 months post-closing

This is a hard negotiation. Sellers do not want to hear that their “contractor” arrangements create a six-figure escrow holdback. But the math is the math, and a sophisticated buyer backed by counsel who understands this exposure has a strong negotiating position.

Voluntary Reclassification Before Closing

The cleanest solution is requiring the seller to reclassify misclassified workers as W-2 employees before closing. The seller can use the IRS Voluntary Classification Settlement Program (VCSP) to prospectively reclassify workers with reduced penalties.

Under the VCSP, the seller pays approximately 10% of the employment tax liability for the most recent year — a fraction of what a full audit assessment would produce. The seller handles the reclassification, absorbs the cost, and you acquire a business with a clean classification profile going forward.

Make this a condition of closing. It is one of the most cost-effective risk mitigation strategies available.

When Misclassification Is a Deal-Breaker

Misclassification alone rarely kills a deal, but it can when combined with other factors:

- More than five misclassified workers across core functions, suggesting a systemic disregard for employment law

- Prior adverse audit findings that were never corrected

- No workers’ comp coverage for workers performing physical funeral home tasks

- Seller refuses to indemnify or reclassify, indicating either dishonesty or an unwillingness to deal fairly

- Exposure exceeds 15–20% of the purchase price, fundamentally altering the economics

If the seller has been running the operation with a workforce that is largely off-books, the compensation structure you inherit will need to be rebuilt from scratch — and the true labor cost of the business is significantly higher than the financials suggest.

Frequently Asked Questions

Can I just reclassify all workers as employees on day one and move on?

You can reclassify going forward, but that does not eliminate liability for the pre-closing period. The IRS and state agencies can still audit the historical classification and assess back taxes against the business entity. Reclassification protects you from future exposure; it does not erase past exposure.

What if the seller used a staffing agency for some workers?

Workers sourced through a legitimate staffing agency are typically employees of the agency, not the funeral home. Verify that the agency is properly licensed, carries workers’ comp, and withholds employment taxes. If the “staffing agency” is a shell entity created by the seller, that arrangement will not survive scrutiny.

Does the ABC test apply in my state?

As of 2026, approximately 30 states use some version of the ABC test for at least some purposes (unemployment insurance, wage and hour, or general employment classification). The National Conference of State Legislatures maintains a current state-by-state summary. Even in states that use the IRS common-law test, funeral home contractor arrangements frequently fail.

How do I estimate the total exposure before making an offer?

Total all 1099 payments over three years. Multiply by 25–35% for combined federal and state tax exposure including penalties. Add 10–15% for interest and potential workers’ comp gaps. That gives you a rough ceiling for your escrow holdback negotiation.

The Bottom Line

Worker misclassification is not a technicality. It is a substantive financial liability that transfers with the business you are buying. The seller saved money for years by avoiding employment taxes. You will pay for those savings if you do not identify the exposure, quantify it, and negotiate accordingly.

Every funeral home acquisition involving 1099 workers deserves a classification audit as part of due diligence. The cost of getting this right before closing is a fraction of what you will pay if the IRS or your state labor department comes calling after.

This guide is part of the Funeral Home Buyer resource library — acquisition intelligence for serious buyers, from due diligence through operations.

Funeral Home Buyer provides educational content for professionals evaluating business acquisitions in the funeral services industry. This article is not legal, financial, or investment advice. Consult qualified professionals before making acquisition decisions.